Every month the Royal Institution of Chartered Surveyors (RICS) releases its UK Residential Market Survey, providing valuable insights into the current state of the housing market nationwide.

This blog post is bought to you by our Chairman & Managing Director, John King, FRICS, who offers valuable insights from his experience here at andrew scott robertson in South West London He actively contributes his comments to the monthly survey for the London region.

KEY OUTTAKES FROM THE FULL RICS RESIDENTIAL MARKET SURVEY FOLLOWING END OF FEBRUARY RESULTS 2024

Residential Sales Market Insights

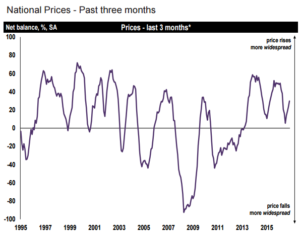

House prices are they going up or down?

The number of residential transactions has substantially increased since the start of the year although no signs of any price increases yet. Indications are that values have stabilised particularly noticeable in the outer suburbs of London. There remains cautious optimism. Falling mortgage rates and a realignment of buyer-seller expectations has contributed to increased market activity.

New instructions

Some vendors seeking to sell have been cautious in not exposing their properties to the market too soon. The process from thinking to sell and placing their property onto the market is a time consuming emotional wrench for most would be sellers. It’s a hand holding exercise for most of us agents when dealing with clients yet to make up their minds.

There’s been a noticeable surge in the number of appraisals giving more confidence to vendors in knowing that buyer registrations remain higher than this period last year. As a rule, spring instructions most often lead to more offers.

New buyer enquiries

However, despite this increased activity, there hasn’t been a corresponding rise in property values. New listings and buyer enquiries generate the most viewings during the first 3 weeks of coming to the market. Properties that linger on the market longer do often struggle as ambitious asking prices discourage potential purchasers in putting forward offers. Buyer registrations have increased with a number having increased their budgets, unable to find the right property.

Agreed sales

A significant increase in sales has occurred since the start of the year driven by more affordable mortgage offers especially in lower price regions ( £500k -£1m) with a natural flow into the middle sectors (£1.5m-£3.5m). This also suggests a growing number of buyers now consider that the cost of stamp duty has aligned itself to vendors expectations.

Lettings market insights

Tenant demand that had seen a modest rise, over the previous quarter but has now subsided as tenants demand better amenities before paying asking rents. Meanwhile, the decline in the number of new landlords entering the market for the first time is beginning to turn as lower interest rates is attracting more interest from this sector. The stock market remains its main competitor.

For more from the RICS UK Monthly Residential Market survey, you can download and read more 2023/2024 reports here: https://www.rics.org/news-insights/market-surveys/uk-residential-market-survey

Please feel free to reach out to us for personalised advice and assistance in this ever-evolving real estate market. Find the right team for your needs here.

Regards,

John King, FRICS